healthcare

Nov 10 2020

Today, the Supreme Court will hear arguments why the Affordable Care Act should be struck down in its entirety versus why it is too important not to continue undisturbed. If the justices decide the former, the consequences will be calamitous.

Almost…

Read More »

healthcare

Oct 17 2020

A week after the election, the Supreme Court will hear arguments why the Affordable Care Act should be struck down in its entirety versus why it is too important not to continue undisturbed. If the…

Read More »

healthcare

Jan 27 2017

On his first full day in the White House, Donald Trump signed an executive order that effectively told all federal agencies to be lax on enforcing provisions of the Affordable Care Act, colloquially known as ObamaCare. That could lead to expanded waivers as tax time nears, reducing the number of people required to pay penalties for not buying insurance. It could mean the health department tipping off insurers that it won't object to lessening coverage provisions in their policies to reduce costs. By law, those waivers can be applied for only in certain periods during the year, and minimum coverage features are baked into the Act, but will agencies reading the order's vigorous instruction to act “to the maximum extent permitted by law” simply look the other way?

Perhaps it was only a gesture by Trump to prove to his following that he will deliver on his promise “to minimize the unwarranted economic and regulatory burdens”, as his order says, on the road to dismantling Obama's major achievement. But given language that is more than a suggestion, telling them to “waive, defer, grant ¬exemptions from or delay”, the agencies may think they had better take action or have to answer to Trump why they did not.

What if, while Republicans scramble to come up with a replacement to substitute for repeal (see related story), the Justice Department takes Trump's order to mean it should drop its defense against the House of Representatives suit against the government that says the subsidies are illegal? The health act provides subsidies to help people buy insurance, but the House never appropriated the money. The suit argues that funds meant for other purposes were misappropriated. The subsidies continue pending appeal, but if Justice drops its appeal, Obamacare's insurance market is sure to collapse.

This intemperate and unnecessary move by the President before any substitute has even been formulated could lead to serious erosion or even destruction of the healthcare act just when the new administration needs to assure the millions now benefiting from insurance that it is not going to be taken away. Instead, Mr. Trump seems to have a preference for chaos.

Comment?

healthcare

Suing for exemption from Obamacare contraceptive coverage

Apr 10 2016

The Supreme Court at the end of March heard seven petitions clustered under Zubik v. Burwell arguing that employers should not be required against their religious principles to facilitate even indirectly contraception for their employees as required of insurance plans by the Affordable Care Act.

Their suits are a follow-on from the Court's decision in favor of the Hobby Lobby corporation, which gave a closely-held family-owned business a special exemption from paying for insurance that includes contraceptives. Doing so, went the plaintiffs argument, offended the religious sensitivities of the corporation. You read that correctly.

Justice Elena Kagan foretold the ruling would bring religious objectors “out of the woodwork”, and here they are — just a fraction, says one…

Read More »

healthcare

It's money that matters

Jan 22 2016

The Affordable Care Act depends on taxes and penalties to pay for the subsidies that help low-income individuals and families buy insurance. But the administration has repeatedly been cavalier about money.

Companies with over 50 employees are required under the Act to pay for insurance for their full-time workers or pay a fine of at least $2,000 and as much as $3,000 per employee. Yet right off, and out of compliance with the ACA statute, the White House issued waivers to several hundred companies — seemingly anyone who asked. Then the employer mandate was postponed for a year to 2015, then postponed another year for companies with 50 to 99 employees, and just recently…

Read More »

healthcare

Will seven words trump the rest of the text?

Jun 21 2015

Should the government be barred from paying subsidies to persons buying health insurance because seven words in the 602-page Affordable Care Act fail to Court OKs Subsidies: June 25: In exactly the 6-3 split that the adjacent article forecast, the Supreme Court has validated the federal government's paying subsidies to those who sign up on the federal exchanges. The justices' logic matches what we set forth here.

mention federal exchanges? Or do other sections of the statute show that phrase to be only a lapse in wording?

So argue the briefs before the Supreme Court in King v. Burwell, the long-awaited case that could cripple Obamacare. The Supreme Court is expected to render its verdict as soon as this Friday.

THE FINE PRINT

For the 34 states unwilling to mount their own exchange, the Affordable Care Act (ACA) provides for the federal government to establish and manage an exchange in their behalf. The text then says that subsidies are to be granted to low-income people who sign up for insurance "through an Exchange established by the State". Missing is any explicit wording that says the federal government is also authorized to pay subsidies to persons who sign up on the exchanges it runs.

A drafting error, say those who insist the mission is the same no matter who administers the exchanges. The obvious intent is for all Americans to be treated equally.

A decision that prohibits the federal government from issuing subsidies to those who signed up on the exchanges it runs would sink Obamacare, which is precisely the objective of the group that searched the Act for an Achilles heel, found those seven words, and sued the government. If denied those subsidies, an estimated eight million could no longer afford the insurance, with only the sickest paying no matter the cost, meaning the insurers will need to spiral premium costs upward to pay for the care of these most expensive policy holders, and that will drive still more people into the uninsured column. This is the downward "death spiral" that the petitioners hope will kill Obamacare.

REACHING FOR IT

It was highly unusual and suspect that the Supreme Court reached for King v. Burwell, in which the 4th Circuit Court of Appeals in Virginia had approved the federal payment of subsidies. There had been no split rulings at the circuit level to cause the highest court to step in.

In a second challenge to the federal subsidies, Halbig v. Burwell, a three-judge panel of the Washington D.C. Circuit Court of Appeals had reached the opposite decision, ruling that the federal-run exchanges could not pay subsidies because of the seven words. But that court had vacated its own ruling, deciding that the case should be heard en banc, that is, by all the judges of that court.

That left King as the only ruling out there when the Supreme Court jumped the line, taking King for itself and thus aborting the D.C. court's review of Halbig.

What was that about? Were the conservative justices wary that seven of D.C.'s eleven judges were appointed by Democratic presidents and might be disposed to rule in favor of the subsidies? If both cases were decided for the administration, the Supreme Court would have no justification to intervene.

This has happened before. It is a reminder of a similar moment when the justices reached well beyond a complaint about a corporate-funded political movie brought by the conservative advocacy organization Citizens United in order to advance a political agenda of unlimited campaign spending by corporations and unions. It's hard not to suspect that the conservative justices again reached for a case because they wanted another crack at Obamacare.

THE CHALLENGE

The King brief relies on the seven words in isolation, in proving that they were deliberate, that the federal government was to be denied issuing subsidies. The intent was to force states to set up their own exchanges.

The brief uses as evidence newspaper articles such as The New York Times saying in 2012 that “lawmakers assumed that every state would set up its own exchange” because “political reality” would deter them from turning down “billions” of free federal dollars. The brief cites Jonathan Gruber, an MIT professor and heavily paid consultant involved in crafting the healthcare bill, who had popped up in videos calling Americans "stupid" for not figuring out that the young and healthy insurance buyers would be paying for the old and sick, but relative to this case had said,

“If you’re a state and you don’t set up an Exchange, that means your citizens don’t get their tax credits.… I hope that that’s a blatant enough political reality that states will get their act together and realize there are billions of dollars at stake here in setting up these Exchanges, and that they’ll do it.”

Plaintiffs argue that it is not exceptional for the government to bestow its largesse only in return for states complying with a federal requirement; one need look no further than Medicaid within the Affordable Care Act itself. The states get 100% funding to cover new applicants for three years, but only if they expand the number of recipients.

Gruber notwithstanding, King's contention that Congress deliberately attempted to coerce the states finds no corroboration from anyone in Congress. If denying subsidies to any state that failed to set up its own exchange had been the expressed intent, would we not have heard of furious arguments in Congress as the bill was formed and debated? Yet there was none. Jeffrey Toobin at the New Yorker says there were 53 meetings of the Senate Finance Committee, seven days of committee debate on amendments, and 25 consecutive days spent by the full Senate on the bill — "the second-longest session ever on a single piece of legislation" — with "similar marathons in the House". Yet in all those deliberations there was no uproar because no one proposed that the subsidies were to be available only on the state exchanges.

THE DEFENSE

The government argues that, given the Court's own prior pronouncements, the full text of a statute must be taken into consideration — so-called "textualism". “When we look at a provision of law, we look at the entire provision of the law," said Justice Antonin Scalia early this year. “We try to make sense of the law as a whole”. Briefs cite his quotes as well as his emphasis on textualism in books he authored. "The interpretation of a law should do least violence to the text”, Scalia has written. In a post on SCOTUSblog, Yale Law School Professor Abbe Gluck said the "textualists" on the Court like Scalia "have spent three decades convincing judges of all political stripes" to adopt holistic readings of the law, giving priority to the full text. Says one brief, "Textualism demands that judges take seriously the statutory design (as gathered from the text) and avoid interpretations that would render the statute unworkable".

The government points to several places in the law that contradict the seven words with wording that assumes the federal government will be paying subsidies. Examples:

The same section that purportedly limits subsidies to states that create their own exchanges calls for both state and government exchanges to provide the IRS with the information it needs to administer the subsidies (they take the form of tax credits). Why would the government exchanges be required to provide that information if none of its customers are eligible for such credits?

The same section that purportedly limits subsidies to states that create their own exchanges calls for both state and government exchanges to provide the IRS with the information it needs to administer the subsidies (they take the form of tax credits). Why would the government exchanges be required to provide that information if none of its customers are eligible for such credits?

The government contends that an exchange it creates for a state is "established by the state", with the government acting in its behalf. Section 1321 prescribes that Health and Human Services “shall...establish and operate such Exchange within the State”. That wording treats the federal exchanges not as federal but as surrogate state exchanges.

Other sections concerning state exchanges make no separate mention of parallel federal exchanges, implying that the Act considers them to be one and the same and that subsidies are therefore intended for both.

Section 1312(f) stipulates that only a person who “resides in the State that established the Exchange” can purchase on an exchange. If a federal exchange established for a state is not considered a state exchange, then that state can have no customers, says this rule. The clear intention is that all such exchanges are considered by the Act as state exchanges and therefore eligible for subsidies.

Three times in the Act, "Exchange" is defined as being a state exchange, the point being that there is no federal exchange, only subsidy-eligible state exchanges run by the federal government.

It was the IRS that decided federal exchange clients would be eligible for subsidies. It is traditional that the interpretation by the agency of government charged with administering a law is given deference — the "Chevron" principle, named for an earlier precedent — one argument the government makes. The petitioners against the federal subsidies argue that the IRS does not have the authority to make so sweeping a revision of so major a statute.

TRICKING THE STATES

The seven words occur in a section of the Act that spells out — in the tangled language familiar to do-it-yourself 1040 filers (e.g., "the amount equal to the lesser of" and "the excess, if any, of") — the rules for who is entitled to a subsidy and how much. Briefs for the government raise a twofold question: first, why would a restriction of such enormity be buried in the formulas of an ancillary, nuts-and-bolts sub-section; and second, why would Congress knowingly build in a provision that has the power to sabotage its own law?

One of the briefs in support of the government was filed by 23 state attorneys from a mix of red and blue states that says the challengers' position would “violate basic principles of cooperative federalism by surprising the states with a dramatic hidden consequence of their exchange election”. The brief assumes that each of the 34 states that elected not to set up an exchange must have deliberated their options, so would they all have decided to let the government run their exchange had they realized that subsidies would be denied to their people? "Nothing in the ACA provided clear notice of that risk", which is a principle of cooperative federalism. "Retroactively imposing such a new condition now would upend the bargain the states thought they had struck”, says the brief.

SWING VOTE

In the March hearing, Justice Anthony Kennedy, the crucial swing vote on the otherwise ideologically polarized court, had something else on his mind. King may only be a case of statutory interpretation, but wouldn't there be constitutional issues if the Court ruled that subsidies were only available to residents of a state that had set up its own exchange? Doesn't that effectively and unconstitutionally coerce the states to fall in line, Kennedy asked, because accepting so severe a penalty on its citizens would not be a “rational choice for a state to make". And how to justify denying them insurance subsidies that other Americans would get? “There is a serious constitutional problem here if we adopt your position,” Kennedy said to Michael Carvin, representing the plaintiffs. That gave hope to those who want Obamacare to go forward undisturbed.

This factors into our prediction at the conclusion of the other article on the subject, for which see "If the Supreme Court Eviscerates Obamacare, Then What?". But one is left to wonder whether the justices actually read the briefs, some of their questions being seemingly superficial. And do they consider the real world consequences of their actions, given that they are personally utterly unaffected. Samuel Alito contended in the hearing that, if the subsidies were denied, "going forward there would be no harm”.

Do any of them realize that, were they to lock onto seven words rather than the rest of the text, the disruption of millions losing their insurance after the disruption of gaining it would place the legitimacy of the Court at risk?

Finally, Jeffery Toobin's fitting observation: "The great Supreme Court cases turn on the majestic ambiguities embedded in the Constitution…. Instead of grandeur, there is a smallness about this lawsuit in every way except in the stakes riding on its outcome".

Comment?

law

A look at the havoc the Supreme Court could wreak

Jun 9 2015

Conservatives are elated by the prospect that the Supreme Court may later this month deal a crippling blow to the Affordable Care Act, otherwise known as Obamacare. Michael Greve, once chairman of the Competitive Enterprise Institute, which has funded the legal assault on the Act, put it this way: “This bastard has to be killed as a matter of political hygiene. I don’t care how this

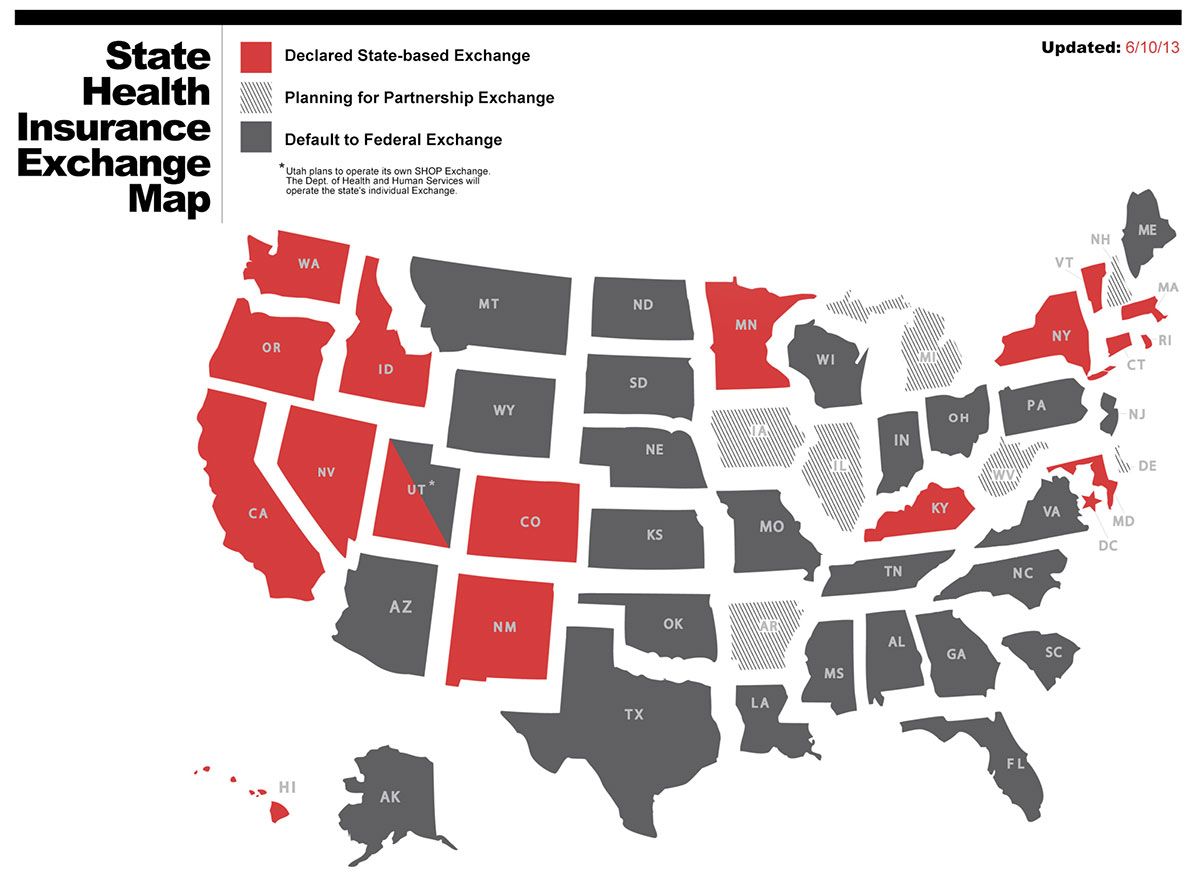

Map shows who runs each

state's exchange. (click image to expand)

is done, whether it’s dismembered, whether we drive a stake through its heart, whether we tar and feather it and drive it out of town, whether we strangle it.”

King v. Burwell is the healthcare law challenge that rests entirely on four words in the 902-page Act — words that, if followed regardless of the rest of the statute, say that the subsidies that make health insurance affordable to the great majority of new policy holders can only be paid to those who buy insurance through an exchange "established by the State".

But 36 states didn't bother to set up insurance exchanges, leaving the chore to the federal government. If a majority of justices say that the four words predominate, that persons who bought insurance on the federal HealthCare.gov site are ineligible for subsidies, then policies are expected to become too expensive for 8 million very angry people come July, with more to join them as premiums soar out of control.

then what?

The President is probably already carrying around in his breast pocket a single-sentence fix for Congress immediately to pass. But passage would require a suddenly forgiving and charitable outlook from a House of Representatives that has voted over 50 times to repeal the healthcare act in its entirety, and a Senate ruled by a majority leader who has said, "I want to pull this law out, root and branch".

At times it seems that the black robes worn by the justices are more like burkas, shielding them from the actual world. How else could Justice Scalia have such faith in that Congress as to ask Solicitor General Donald Verrilli, who argued for the government in the March hearings, "You really think Congress is just going to sit there while all of these disastrous consequences ensue?". And Justice Alito assumed, "It's not too late for a state to establish an exchange" — in all 36 states evidently and in time for the Court's adverse ruling — "so there would be no harm going forward".

sitting on their hands

The Obama administration's attitude is that, if conservatives want to eviscerate the law, then it's for them to deal with the fallout. Sylvia Burwell, who as Secretary of Health and Human Services is the defendant in King v. Burwell, has said, "We know of no administrative actions that could, and therefore we have no plans that would, undo the massive damage …that would be caused" by a decision against the administration. Besides, were the administration to scurry about, positing solutions, it might work against them because it would say to the Supreme Court that there are viable alternatives, so go do your worst.

Twenty-five days is the traditionally expected time after a court ruling that it is to take effect. It is then that the government would have to stop sending tax credits to the insurance companies, which would begin billing policy holders the full cost. They are for the most part lower- to middle-income families, working part time or full. More than 80% receiving

|

As the estimated 8 million drop out of the insurance pool, those who stay in will tend to be the less healthy who need coverage. Insurers will have to raise their rates to pay for the care of these more costly people — one estimate says an increase of 35% in 2016 to begin with — and the higher rates will cause still more to drop away. The so-called "death spiral" is set in motion as the ever rising rates drive out still more policyholders leaving behind all but the sickest and most expensive, causing rates to rise further and still more abandoning insurance. Insurance companies finally pull out of the markets and the exchanges collapse. "

|

subsidies fit this profile

and for them an outsized medical cost would be devastating. Subsidies pay for an average of 72% of their insurance costs, according to administration officials, meaning that policy costs would almost quadruple if the Court shuts off subsidies. That would set in motion the feared "death spiral" [sidebar] that will collapse the Affordable Care Act.

That is, unless the administration adopts one imaginative strategy put forth by William Baude, an assistant professor of law at the University of Chicago: he suggests the administration "announce that it is complying with the Supreme Court’s judgment — but only with respect to the four plaintiffs who brought the suit". They do not represent anyone other than themselves. Pay them their minuscule damages and be done with it. It took some doing to line up these four. Who else would sue because they had been paid subsidies?

squeeze play

Ironically, it will be Republican governors who will experience the most acute pressure. It is they, holding the governorship in 37 states, who account for most of the 36 states that, in defiance of Obamacare, did not set up exchanges in their states.

The Obama camp will pressure them to do so now, or might devise a dodgy workaround for them to adopt their state's federal exchange as their own, so that it would become eligible to issue subsidies. If they go along, those governors can expect to be pilloried within their party for further embedding the Affordable Care Act. If they don't, they will face the wrath of their irate citizens who, as the consequence of no state exchange, will lose insurance that has become too costly without the subsidies, and face as well the disaster this will be for the insurance markets in their states when all those policies evaporate.

Foreseeing this outcome perhaps explains why 31 of those governors did not file amicus briefs with the Supreme Court urging a decision against the administration. A number did the opposite, asking the High Court to preserve the subsidies their residents get through HealthCare.gov. The Affordable Care Act's Medicaid expansion offers an example of what might be on the horizon. Since 2012 some 28 states have joined new Medicaid. Eight more are considering, even holdout Florida. If the same pattern emerges with states setting up insurance exchanges, Republicans will witness a slow-motion defeat.

replace and repeal

But Congress has other plans. Republicans will spring to action the moment the gavel comes down on a decision that forbids subsidies for insurance bought on federal exchanges. No end of bills await the moment, whether the one by Senators Richard Burr of North Carolina, Utah's Orrin Hatch and Representative Fred Upton of Michigan, or from freshman Senator Ben Sasse of Nebraska or by Ron Johnson, senator from Wisconsin, to select only three.

All plans would extend subsidies into 2017 to avoid voter repercussions of cutting them off before an election year. They would variously offer a permanent program of tax credits (the form that subsidies take) to help pay for insurance, scaled downward as income rises (Burr-Hatch-Upton); block new applicants from receiving subsidies but keep them flowing to current enrollees at current levels until August 2017 and then end them cold turkey (Johnson); or cut them to 65% of current levels and phase them out by 5% a month until they are extinguished (Sasse).

What all have in common is abolishing both the individual mandate that requires individuals to buy insurance or pay penalties, the mandate that requires employers of over 50 people to buy insurance for them, and the federally mandated minimal insurance plans. States would be freed to develop their own reduced criteria to make insurance more affordable. Insurers could compete across state borders.

But all would keep the Obamacare provisions that coverage include family members up to age 26, that insurers must accept applicants with pre-existing conditions, that insurers cannot cancel policies when subscribers fall ill. That led Paul Waldman of the The American Prospect to observe "something remarkable" on Washington Post online, that "for all the claims we'll hear about how it undoes the tyrannical horror of Obamacare, the Republicans’ version of health care reform" is "little more than Obamacare Lite…This tells us that Barack Obama has for all intents and purposes won the health-care argument".

None of the reform plans seem to confront the question of what happens to premiums for the rest if the healthy are free not to buy in. Perhaps inducing the death spiral is the unmentioned intent: eliminate the rules to undermine the tenuous structure crafted to make all the parts of the Affordable Care Act come together to work financially so that eventually the last vestiges of the Obamacare design collapse. Then, once a Republican president is installed come January 2017, with Republican control retained in both houses of Congress, what's left of the Affordable Care Act can finally be repealed.

What will work for the Republicans when these bills come up for a vote is that blame will shift to the President when he vetoes them. They preserve federal subsidies at least for a time and it will now be Obama who will have made insurance unaffordable by refusing any encroachment on his grand healthcare design.

But legislation may never reach that stage. Arch conservatives in groups such as the House Freedom Caucus with over 30 members, fronted by Jim Jordan (R-Oh), simply want the subsidies to end with no soft landing and will work to block passage in the House.

won't happen

But we'll go out on a limb and say that none of the above will happen, that the Supreme Court will vote 6 to 3 that subsidies may be paid to those who buy insurance through the federally managed exchange.

Three — Scalia, Alito and Thomas — will assuredly vote against the administration. Despite Scalia's lecture on the philosophy of "textualism" (see "Will the Supreme Court Cripple Obamacare?"), he and they will fasten on the four little words.

Four — Ginsburg, Breyer, Kagan and Sotomayor — will assuredly vote for the administration's position.

That leaves Kennedy and Roberts. Kennedy surprised listeners in the March hearings with his concerns that there may be constitutional issues in effectively coercing states to set up exchanges else see their citizens lose benefits that will be granted to other states that fall in line. It is hard to see how he can go back on that and explain away those concerns, so our guess is that he will side with the government.

Thus deadlocked at 4 and 4, how will Chief Justice Roberts vote? He might yearn to make amends with the conservative base after letting the individual mandate go forward, classifying it as a "tax", when he could have delivered a death blow to Obamacare, killing it in its crib.

But would he really be so blinkered as to lock onto four words in the text, ignoring the rest of the Act, several sections of which make clear that availability of subsidies for all who qualify economically was the intent? Is that cramped interpretation what he wants as the legacy of the Roberts court?

With the disastrous Citizens United decision already in his record, does he now want to author the chaos that will ensue if four words are allowed to disembowel the healthcare law? Or will he take note of what Judge Andre Davis said to the King attorney in oral arguments before the federal appeals court in Virginia that led to the Supreme Court taking up the case: “You are asking us to kick millions of Americans off health insurance just to save four people a few dollars?”

1 Comment

healthcare

In the hearing March 4, justices displayed their usual partisan split

Mar 10 2015

Should the government be barred from paying subsidies to persons buying health insurance because

seven words in the 602-page Affordable Care Act fail to mention federal exchanges? Or do other sections of the statute show that phrase to be only a lapse in wording?

So argued the briefs before the Supreme Court in King v. Burwell, the long-awaited case that could cripple Obamacare that was heard March 4th.

But as something of a surprise, Justice Anthony Kennedy, the crucial swing vote on the otherwise ideologically polarized court, had something else on his mind. King may only be a case of statutory interpretation, but wouldn't there be constitutional issues if the Court ruled that subsidies were only available to residents of a state that had set up its own exchange, Kennedy asked? Doesn't that effectively and unconstitutionally coerce the states to fall in line, because accepting so severe a penalty on its citizens would not be a “rational choice for a state to make". And how to justify denying them insurance subsidies that other Americans would get? “There is a serious constitutional problem here if we adopt your position,” Kennedy said to Michael Carvin, representing the plaintiffs.

If that gave hope to those who want Obamacare to go forward undisturbed, it needs to be mentioned that Kennedy also challenged Solicitor General Donald Verrilli, arguing for the administration.

the fine print

For states unwilling to mount their own exchange — 34 of them, as it has turned out — the Affordable Care Act (ACA) provides for the federal government to establish and manage an exchange in their behalf. The text then says that subsidies are to be granted to low-income people who sign up for insurance "through an Exchange established by the State" — the notorious seven words. Missing is any explicit wording that says the federal government is also authorized to pay subsidies to persons who sign up on the federally run exchanges

A drafting error, say those who insist the mission is the same no matter who administers the exchanges. The obvious intent is for all Americans to be treated equally.

A decision that prohibits the federal government from issuing subsidies to those who signed up on the exchanges it runs would sink Obamacare, which is precisely the objective of the group that searched the Act for an Achilles heel, found those seven words, and sued the government. If denied those subsidies, an estimated seven million could no longer afford the insurance, with only the sickest paying no matter the cost, meaning the insurers will need to spiral premium costs upward to pay for the care of these most expensive policy holders, and that will drive still more people into the uninsured column. This is the downward "death spiral" that the petitioners hope will kill Obamacare.

reaching for it

It was highly unusual and suspect that the Supreme Court reached for King v. Burwell, in which the 4th Circuit Court of Appeals in Virginia had approved the federal payment of subsidies. There had been no split rulings at the circuit level to cause the highest court to step in.

There had been. In a second challenge to the federal subsidies, Halbig v. Burwell, a three-judge panel of the Washington D.C. Circuit Court of Appeals had reached the opposite decision, ruling that the federal-run exchanges could not pay subsidies because of the seven words. But that court had vacated its own ruling, deciding that the case should be heard en banc, that is, by all the judges of that court.

That left King as the only ruling out there when the Supreme Court jumped the line, taking King for itself and thus aborting the D.C. court's review of Halbig.

What was that about? Were the conservative justices wary that seven of D.C.'s eleven judges were appointed by Democratic presidents and might be disposed to rule in favor of the subsidies? If both cases were decided for the administration, the Supreme Court would have no justification to intervene.

This has happened before. It is a reminder of a similar moment when the justices reached well beyond a complaint about a corporate-funded political movie brought by the conservative advocacy organization Citizens United in order to advance a political agenda of unlimited campaign spending by corporations and unions. It's hard not to suspect that the conservative justices again reached for a case because they wanted another crack at Obamacare.

the challenge

The King brief relies on the seven words in isolation, in proving that they were deliberate, that the federal government was to be denied issuing subsidies, and that adhering to those words does not render other sections of the act "absurd". The intent was to force states to set up their own exchanges.

The brief uses as evidence newspaper articles such as The New York Times saying in 2012 that “lawmakers assumed that every state would set up its own exchange” because “political reality” would deter them from turning down “billions” of free federal dollars. The brief cites Jonathan Gruber, an MIT professor and heavily paid consultant involved in crafting the healthcare bill, who had popped up in videos calling Americans "stupid" for not figuring out that the young and healthy insurance buyers would be paying for the old and sick, but relative to this case had said,

“[I]f you’re a state and you don’t set up an Exchange, that means your citizens don’t get their tax credits.… I hope that that’s a blatant enough political reality that states will get their act together and realize there are billions of dollars at stake here in setting up these Exchanges, and that they’ll do it.”

Plaintiffs argue that it is not exceptional for the government to bestow its largesse only in return for states complying with a federal requirement; one need look no further than Medicaid within the Affordable Care Act itself. The states get 100% funding to cover new applicants for three years, but only if they expand the number of recipients.

Gruber notwithstanding, King's contention that Congress deliberately attempted to coerce the states finds no corroboration from anyone in Congress. If denying subsidies to any state that failed to set up its own exchange had been the expressed intent, would we not have heard of furious argument in Congress as the bill was formed and debated? Yet there was none. Jeffrey Toobin at the New Yorker says there were 53 meetings of the Senate Finance Committee, seven days of committee debate on amendments, and 25 consecutive days spent by the full Senate on the bill — "the second-longest session ever on a single piece of legislation" — with "similar marathons in the House". Yet in all those deliberations there was no uproar because no one proposed that the subsidies were to be available only on the state exchanges.

the defense

The government argues that, given the Court's own prior pronouncements, the full text of a statute must be taken into consideration — so-called "textualism". “When we look at a provision of law, we look at the entire provision of the law," said Justice Antonin Scalia just two months ago. “We try to make sense of the law as a whole”. Justice Kennedy in a 2006 opinion had said that a particular provision of a law being reviewed was persuasive only "without the illumination of the rest of the statute". Briefs cite these quotes as well as Scalia's emphasis on textualism in books he had authored. "The interpretation of a law should do “least violence to the text”, Scalia has written. In a post on SCOTUSblog, Yale Law School Professor Abbe Gluck said the "textualists" on the Court like Scalia "have spent three decades convincing judges of all political stripes" to adopt holistic readings of the law, giving priority to the full text. Says one brief, "Textualism demands that judges take seriously the statutory design (as gathered from the text) and avoid interpretations that would render the statute unworkable".

The government points to several places in the law that contradict the seven words with wording that assumes the federal government will be paying subsidies. Examples:

The same section that purportedly limits subsidies to states that create their own exchanges calls for both state and government exchanges to provide the IRS with the information it needs to administer the subsidies (they take the form of tax credits). Why would the government exchanges be required to provide that information if none of its customers are eligible for such credits in the first place?

The government contends that an exchange it creates for a state is "established by the state", with the government acting in its behalf. Section 1321 prescribes that Health and Human Services “shall...establish and operate such Exchange within the State”. That wording treats the federal exchanges not as federal but as surrogate state exchanges.

Other sections concerning state exchanges make no separate mention of parallel federal exchanges, which means that the Act considers them to be one and the same — and that subsidies are therefore intended for both.

Section 1312(f) stipulates that only a person who “resides in the State that established the Exchange” can purchase on an exchange. If a federal exchange established for a state is not considered a state exchange, then it can have no customers, says this rule. The clear intention is that all such exchanges are considered by the Act as state exchanges and therefore eligible for subsidies.

Three times in the Act, "Exchange" is defined as being a state exchange, the point being that there is no federal exchange, only subsidy-eligible state exchanges run by the federal government.

It is the IRS that promulgated the "rule" that the federal exchange clients would be eligible for subsidies. It is traditional that the interpretation by the agency of government that is charged with administering a law is given deference — the "Chevron" principle, named for an earlier precedent. The petitioners argue that the IRS does not have the authority to make so sweeping a revision of so major a statute — a valid point, but seemingly lost in the cascade of other arguments by both sides.

tricking the states

The seven words occur in a section of the Act that spells out — in language familiar to do-it-yourself 1040 filers such as "the amount equal to the lesser of" and "the excess (if any) of" — the rules for who is entitled to a subsidy and how much. Briefs for the government raise a twofold question: first, why would a restriction of such enormity be buried in the formulas of an ancillary, nuts-and-bolts sub-section; and second, why would Congress knowingly build in a provision that has the power to sabotage its own law?

One of the briefs in support of the government was filed by 23 state attorneys from a mix of red and blue states that says the challengers' position would “violate basic principles of cooperative federalism by surprising the states with a dramatic hidden consequence of their exchange election”. The brief assumes that each of the 34 states that elected not to set up an exchange must have deliberated their options, so would they all have decided to let the government run their exchange had they realized that subsidies would be denied their people? "Nothing in the ACA provided clear notice of that risk", which is a principle of cooperative federalism. "Retroactively imposing such a new condition now would upend the bargain the states thought they had struck”, says the brief.

outcome

But one is left to wonder whether the justices actually read the briefs, some of their questions being seemingly superficial. And do they consider the real world consequences of their actions, given that they are personally utterly unaffected. Samuel Alito contended in the hearing that, if the subsidies were denied, "going forward there would be no harm”.

Do any of them realize that, were they to lock onto seven words rather than the rest of the text, the disruption of millions losing their insurance and being wrenched about yet again would place the legitimacy of the Court at risk? Chief Justice Roberts was almost completely silent in the hearing, perhaps wondering what would be history's verdict for his Court were it to decide against the government.

Finally, Jeffery Toobin's fitting observation: "The great Supreme Court cases turn on the majestic ambiguities embedded in the Constitution…. Instead of grandeur, there is a smallness about this lawsuit in every way except in the stakes riding on its outcome".

1 Comment

healthcare

An existential threat lurks in the wording of the law

Sep 27 2014

Supremes Take the Case: Nov. 10: As we assumed, the Supreme Court will hear the controversial question of whether the government can offer subsidies to those using the federal exchange. The following article from September explains.

Lawsuits, four in total, are wending their way through the appeals system and one, or their composite, is sure to arrive on the steps of the Supreme Court. They are based on a flaw in the…

Read More »

healthcare

Do corporations have religious rights?

Jan 1 2014

A flock of companies — 84 says the Wall Street Journal — have sued the government arguing that for religious reasons they should not be required by the Affordable Care Act to provide insurance to their employees that includes Sotomayor Issues Decree: Jan 1: The stay issued by the Supreme Court justice on New Year's Eve that temporarily relieved Catholic groups from having to provide insurance that pays for contraceptive aids shows where this case is headed. The White House has asked the Supreme Court to override this peremptory exemption from health care the law in a case yet to be decided.

coverage for contraceptives. The Supreme Court has agreed to hear a pair of such cases combined into one.

If the Court — six of whom are Catholic — decides in favor of these complaints, they will be effectively expanding on their ruling in Citizens United…

Read More »

health care

Nov 5 2013

Republicans called the Affordable Care Act a “train wreck” well before it left the station but the sputtering web engine has made it clear that Obama's administration doesn’t know how to run a railroad.

The website's dysfunction persists but the topic has shifted to the president's shiftiness in telling the public they will be able to keep the insurance plan they have and therefore their same doctors. As many as 10 million of the 15.4 million policies bought by individuals directly…

Read More »

health care

Trouble beyond the easy fixes

Oct 24 2013

Republicans have for weeks been calling the Affordable Care Act a “train wreck” well before it had even left the station but the sputtering October 1 debut made it clear that Obama doesn’t know how to run the railroad.

You’ve got to wonder, how could the President have paid so little attention to the status of what is endlessly called his “signature” achievement that he would say on the same day the government’s Internet insurance exchange crashed that people will be able to shop "the same way you'd order a plane ticket on Kayak or a TV on Amazon".

Instead, the insurance "marketplace" was let loose for the entire country to beta test, but Obama has "brought in some of the best IT experts from across the country" to deal with the emergency, says a White House e-mail, experts who should have been involved from the beginning. Almost three weeks after launch, Obama said in a Rose Garden appearance, "Nobody's madder than me about the fact that the website isn't working as well as it should, which means, it's gonna get fixed", as if the commander in chief can simply order millions of lines of code to rearrange themselves. Most predictions expect that repairs will take weeks. Our forecast is months, and that could bring Obamacare down.

famously aloofDid Obama simply take the word of equally non-technical Health & Human Services (HHS) chief Kathleen Sebelius (a former governor) that “we’re on target”, as she said in a July interview after months of “projecting optimism and confidence”?

Sebelius would soon exhibit cluelessness of her own. A week after the government’s exchange opened, when asked by Jon Stewart on the Daily Show, "How many have signed up thus far?”, she answered, “Fully enrolled, I can’t tell you. I don’t know”. We are now told that in the months before the system would debut, she reportedly misallocated her time traveling the country to promote it, instead of constantly monitoring the progress of the hugely complex system, which could have headed off the disastrous launch. There are calls for madam secretary to resign, as the one ultimately responsible for the botched system, but Obama cannot allow that. Republicans in the Senate would block any nominee he put forward, leaving the department headless.

overflow

Fourteen states either couldn’t be bothered to roll their own system or preferred to undermine Obamacare by not cooperating, leaving the federal government to handle the exchanges for the rest of the states. Visions of deluge should have panicked the Obama administration. Ms Sebelius said that the website’s inability to handle the load would not have occurred “unless millions of people flooded the marketplace”. Surprise! There are millions in the 36 states. So there were 9.5 million visitors in the first week and 4.1 million in the second.

States were better prepared. New York dealt with about 2 million visits in its first 90 minutes; California recorded 5 million on opening day. The HHS secretary belatedly concluded, “We didn’t have enough testing, specifically for high volumes, for a very complicated project.” Ya think?

Months before, they could have found a hacker to launch a distributed denial-of-service attack to bombard the prototype exchange website with increasing loads of millions of logon to reveal at what point the system breaks. They would have discovered well in advance that another warehouse of servers was needed.

Actually, Secretary Sebelius did say that the system had been stress tested. They had set the bar at five times the highest volume that the Medicare.gov website had ever experienced. But Medicare’s universe is only a slice of the population, and when would millions of seniors have had cause to rush that mature system to make for a comparable peak day?

Capacity was only the first problem to surface. USA Today quoted several experts who found evidence of what they said looked like 10-year old web technology, although some of their expertise seems a bit ancient itself, as with one expert’s suggestion that, "If I was them [sic], and I'm just conjecturing, I would probably come up with some manual way of saying, 'Only people with the last name starting with 'A' can sign up today".

remember ‘user friendly’?

Once inside the system, applicants were forced to set up an account before they even decided whether or not they were customers. There was no ability to browse the offerings. That says there was no move to draw on the wealth of technical and marketing savvy of online sellers like Amazon, or to learn from Massachusetts' “Romneycare”, which could have told the system architects that people in that state went online 18 times before they bought insurance. People shop before they buy. At least that design flaw was quickly fixed.

coding confusion

Further in, applicants found a loosely coded site that lacked error checking. One could enter multiple spouses, could list spouses as children, could sign up for more than one plan, could even change someone else's data, could enroll more than once — which happened often when users repeatedly hit the “Submit” button in the unresponsive system.

Much of this is attributable to reports that government officials made constant changes requiring re-writing of code which foreshortened the time remaining for testing in the months leading to the October 1 deadline.

One consequence is flawed data being handed to the insurance companies that are “straining their ability to handle even the trickle of enrollees who have gotten through so far”. Insurers are finding they have to correct a high percentage of submissions manually and even hire temporary workers to phone applicants. They fear an inability to handle the load once the current trickle turns into a flood.

Their bigger worry is that if system problems cannot be rapidly corrected, only the sickest will persevere to buy insurance, whereas the young and healthy — whose participation is key to offsetting the cost of those with illnesses — will give it a try but not come back.

original sin

HHS let the principal contract to the U.S. arm of a Canadian company to create the system. The original bid was $55.7 million, with a cap of $94 million. But those numbers expanded grotesquely, evidencing how badly both the agency and the company underestimated the task before them. Ultimately, $394 million was spent, according to the Associated Press.

The government unaccountably failed to tap the best developers of Internet technology, instead contracting with a company that calls itself an “information technology and business process services firm”, which sounds more like a back office mainframe shop. The hundreds of millions spent on a flawed system bring to mind the decade-long $450 million FBI attempt to modernize its system. Was the HHS the victim of lowest bidder rules and made to chose the wrong supplier?

tangled web

When Congress creates laws, its members seem utterly unmindful and unconcerned for how those laws will be implemented. That is certainly the case with the Affordable Care Act, routinely spoken of as 2,200 pages that no one in Congress ever read (actually, that would be the double-spaced original; the law, as passed, runs to 906 pages and can be found here). Like tax law, it is larded with requirements, many of which are inconsequential, simply adding to complexity. Government departments and agencies are then left to deal with the mess.

Example enough was in a Wall Street Journal column that said, “The Government Accountability Office last year calculated that for the IRS alone, implementing ObamaCare would be a ‘massive undertaking that involves 47 different statutory provisions and extensive coordination’". There is exaggeration in saying that though, because as soon as a few facts are obtained from an applicant’s entries — income above a certain amount, for example — none of the more extensive checks concerning eligibility for subsidies need be made. Only a percentage of applicants need the full bore analysis.

What undoubtedly makes the system frighteningly complex is not the logic paths that the code must follow to gather its information, but the connections it must make. When the code knows at a certain point to reach out to a particular federal database, it may find that its target runs on a different and incompatible platform — a stumbling block that the industry calls “interoperability”. As the clock ticked, system designers had to coordinate with that agency or department to find a way into that database, and if lacking, wait for it to be developed. That external data fiefdom will have its own validating ID, password protocols and data format to work through. Worst of all, the target system may itself not have been engineered to handle heavy loads; there may be bottlenecks all over the network and, if so, they will take a long time to rework.

The need for such coordination, multiplied times the number of external contact points that could be needed for the universe of applicants, makes for a very tangled web. It is our guess that here lies the deeper problems that could take a very long time to straighten out, which is why we said months, not weeks. Our diagnosis

was hinted at by one repair technician quoted in The New York Times who said, “the account creation and registration problems are masking the problems that will happen later".

Comment?