Taxes in America: A Mess That Has Only Grown Worse

Jan 14 2019The tax cuts enacted a year ago by the Republican-controlled Congress and signed by President Trump have inspired a growing realization that America's tax system is a shambles. That verdict goes beyond the uproar over the new tax law handing corporations a 40% rate reduction and the uncalled-for tax cut benefiting the rich. The dog's breakfast resulting from what politicians and special interests have dumped into the tax code across decades with no sense of a master plan has led to a growing consensus that we are doing it all wrong.

In the United States, unlike several European countries, assets are not taxed, no matter how much they may have gained in value, until sold. Most of the wealth the richest Americans have acquired is not taxed, even as it has grown in value from year to year. On the other hand, Congress sees fit in the laws it passes to withhold taxes from the first dollar earned by every salaried worker and every dollar thereafter.

Leaving assets free from from taxation leads to easily the most deviant and insupportable tax practice: the estate and gift tax, which, save for the rare exception, taxes no one by allowing accumulated value to pass on to others tax free. Not only that, but the inheritor's cost basis becomes the value of the asset on the day it has transferred. A giftee could sell stock the day received and pay no tax whatever, no matter by how much the asset had gained in value in the years leading up to the transfer. Or sell the property later — land, securities, whatever — and pay tax only on the difference between the selling price and the phony "cost basis" valuation of the transfer date.

how the rich got richer

In the early 1990s, 18 extremely

wealthy families pooled $500 million to lobby against the tax — the owners of the first and third largest privately held companies (Koch Industries and Mars candy); the family that owned 40% of Walmart; another family owning 40% of Campbell Soup, among them. Legislators benefiting from corporate money flowing into their campaigns were only too happy to oblige.

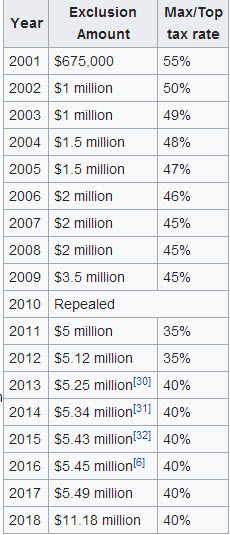

The table shows that as recently as 2001 only the first $675,000 of value in an estate was exempt from the inheritance tax, with a 55% tax rate on amounts above that threshold. In the end- 2017 tax bill, that not only rocketed to $11.18 million that an individual can transfer as gift or on death — and double that for a married couple — but the top tax rate even declined to 40%.. The number of people subject to estate and gift taxes has become so rarified that only about 2,000 (or 0.0006% of the population) in the U.S. are currently liable for the estate tax.

The question: How do the nation's wealthy, and the Congress members who carry water for them, justify imposing no tax whatever when an estate is transferred? We should eliminate the rule that allows all taxable gains to be wiped out at death.

That would be "double taxation" say those who fight what they call the "death tax" and call for what remains of the tax to be repealed altogether. Selling the notion that taxes have already been paid on the income in an estate is a lie that has sold well. Heads nod in agreement, with no thought given to the likely appreciation in value of those assets — real estate, collections, securities, and so on. The tax law looks the other way for this privileged class while the rest of us — the middle-class with its modest income who have to sell things to meet household and educational needs for our kids — are required to pay taxes on whatever gains we realize.

Lobbying campaigns against the estate and gift tax paint a tale of woe every time the subject is raised about offspring having to sell the family farm they have inherited in order to pay the tax. But that's a red herring. For those lacking the cash or unable to borrow, the government could be the lender with a lien, at interest, on illiquid assets payable when an asset — such as that totemic farm — is someday sold. But the tiny violin playing for this equally tiny minority as a basis for foregoing taxes altogether for a huge majority is obviously a sham that doesn't have the country in mind.

There is also the indefensible deduction of the appreciated value of assets when given as family or charitable gifts. That painting you bought fifteen years ago for $2,000, now appraised at $50,000 because the artist has become recognized? You can give that to a charity and subtract the full $50,000 from income that would otherwise be taxed. The same with securities, or anything you give. You have done nothing to make the asset's value appreciate. The outside world's good opinion of it did that. Why the tax giveaway?

And when a gift is made, say to one's children, their cost basis for when they someday sell it, is the value of the asset on the date of the transfer. So that stock held by mom and dad for 10 years that doubled in value, their whole capital gain moves on, tax free.

charity tilted to the richCharitable giving is given a similar free pass. By that we're not referring to modest giving; that's no longer deductible on its own because it is subsumed by the new tax law which doubled the standard deduction. So it is only the biggest givers that get tax deductions. Every tax waiver the government grants for a gift to charity means money the government has to get from the ordinary citizenry. In the next 20 years baby boomers are expected to give almost $7 trillion to philanthropy. Those gifts of millions to Yale or Stanford, reducing by that amount the donor's income that will be taxed, means governments will be squeezed enough to ask the rest of us for more. Does this make sense? Shouldn't philanthropy be limited?

foresight turned offWhat was originally billed as tax reform and simplification, the Tax Cuts and Jobs Act became the opposite, adding new levels of complications. Consider this: Millions of people set up their businesses as limited liability companies, S corporations and partnerships whereby the businesses don't pay the taxes, their profits or losses pass through to owners' personal tax returns. The attraction for using that business form was that those owners mostly paid personal taxes at rates well under the 35% formerly paid by the standalone "C" corporations.

Then came the corporate plan to cut the tax rate from 35% to 21% for corporations. What about everyone with "pass-through" businesses. It was belatedly realized that the tax rate for a subset of millions of businesses would be more than the new 21% tax rate for standalone corporations. It was as if no one in Congress had thought ahead. Something had to be done.

Hurriedly and awkwardly, Congress devised a tax break they thought commensurate with the windfall standalone corporations were getting. This became a clumsy 20% off-the-top deduction from income with tax computed on the balance. There's more. The deduction phases out on income in excess of beyond one dollar level for a single filer, and another for joint filers. And it ends in 2025. And it's not for everyone. An arbitrary list took shape deciding who should be eligible for the discount — flower stores yes, architects no, and so on — arbitrarily based on whether a business has employees. Congress, which had preached simplification as a prime criterion for tax "reform" instead added this and hideous level of jury-rigged complication to a tax code that by 2014 ran to about 2,600 pages but is so complicated that 73,594 pages are needed to explain it.

By the way, those pass-through businesses? Donald Trump reportedly has hundreds of them, each holding ownership of separate real estate undertakings. But they don't have employees so they're not eligible for the 20% deduction, right? At close to the last minute, Utah's Senator Orrin Hatch, quite on his own, without the knowledge of others, "air-dropped" into the bill text that permitted pass-throughs with few or no employees to partake of the deduction, too. This had nothing to do with Trump, of course.

debtThe Economist said a few years back that, "The field for the title of world’s worst economic distortion is a crowded one", and put the subsidization of debt at the top. Economists in general disfavor that governments allow the deduction of mortgage interest, reducing income that is taxed. It is effectively a subsidy to the housing industry, which — no question — would suffer from its elimination as would a margin of people who could no longer afford to buy houses.

The 2017 tax act did take steps, wiping out deduction of interest of home equity loans and capping deductibility at the interest on $1 million in debt, and the interest on $750,000 for newly bought houses — a new complication for homeowners to learn how to compute. But note that the unexplained doubling of the standard deduction to $24,000 a year for marrieds is something of a ruse, covering as it does much or all of what in prior years was homeowners' biggest item in their itemized deduction list. Just as before.

The act also puts partial limits on the interest deduction for businesses, but only for those with three years of gross receipts averaging over $25 million, and it adds a thicket of complications for the rest. Again, so much for simplification.

But the other atrocity in the tax code is the handout to the real estate industry which thinks anyone who winds up with taxable income a fool. The government allows real estate companies to write down the value of a property over as little as 25 years. A property owner thus says that the value of a building declines year-by-year by 1/25th because after 25 years it will be a pile of worthless rubble. That 1/25th is a million dollars for a $25 million property to make the point that these are big bucks reducing profits and therefore taxes throughout the real estate industry even though there is no actual dollar cost and the depreciation is imaginary — just a green-eyeshade entry in a ledger. Why imaginary? Because buildings last far longer — think of apartment buildings in New York City over a hundred years old — and generally increase in value. It is a senseless tax policy, obviously perpetuated by politicians eager for rewards from the real estate industry.

other ideasThere is much more that is wrong, of course. The double taxation of dividends, for instance, or that the idle income of capital gains is taxed at a fixed low rate whereas the tax on labor rises with income, etc.

The inequities of a tax code shot through with illogic has attracted a growing body of true reformers who go beyond just fixing what we cite above and who rethink taxing fundamentally. The most radical ideas come in a book by E. Glen Weyl, chief economist at Microsoft, and Eric Posner of the University of Chicago. They don't at all follow in the footsteps of that university's Milton Friedman. Weyl and Posner would break the iron grip of the property rights so fundamental to conservatives but which they say prevent markets from being truly free.

Take land as representative. It is monopolistic. Its owners block out entry by anyone else. That stymies what might be done with idle land by others who might bring entrepreneurial energy — an apartment building, say, or a business complex. For all property, not just land, the duo promotes a wealth tax. All persons would ascribe a value to everything they own and would be taxed on their self-declared total wealth. The catch is that every item must be available for purchase at its declared value. Pricing an item too low to minimize taxes would attract buyers who will have the right to claim and take possession of the item for that price. So to keep property, an owner would need to ascribe a high value to it — and pay heavy taxes. That at least compensates society for impeding the more constructive use of an asset.

It's an interesting idea that will never happen, but that's true of any change for as long as the current campaign finance laws and the Citizens United Supreme Court ruling allows politicians to follow the money instead of fixing the country.

Please subscribe if you haven't, or post a comment below about this article, or

click here to go to our front page.